Earlier this month, perhaps the most well-known P2P lending platform, Lending Club (LC), issued its quarterly earnings report, which showed that its second-quarter net loss increased from US$4.1 million to US$81.4 million. The company also announced that CFO Carrie Dolan has left the company and the chief financial officer has temporarily taken over.

In the recent May, LC co-founder and CEO Renaud Laplanche resigned because of corporate data fraud, fraud to investors, and the CEO himself did not disclose a conflict of interest investment.

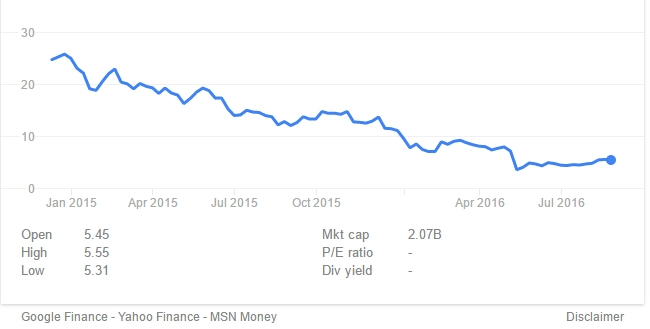

At the beginning of the end of 2014, LC was not only honored as the most important company in the field of financial technology, but also spurred the emergence of domestic P2P lending platforms across the border. By March this year, 3984 P2P lending companies had been established in China. At that time, the LC stock price rose to 29 US dollars, but now it is less than 6 US dollars.

Since the listing of LC shares, pictures from Google

The crisis of LC has only come out recently, but perhaps the early hidden dangers have already been laid. According to a Bloomberg report, the situation of early brushing by LC employees was not new, and the review of loans was not as strict as claimed. This star company has a disgraceful past.

Once invincible

At the beginning of LC, it was considered EBay in the lending sector. It is not the first P2P lending company, but its interest rate setting algorithm and SEC approval make it stand out. Other companies have also begun to imitate the model principle of LC and used it in fields such as real estate, medical care, and even weddings.

After receiving the loan application, LC will use the FICO credit score to use its own risk control model to review the lender and quickly decide whether to lend. It divides the borrower's credit rating into 7 levels, ranging from A to G, and pricing based on risk differences. For borrowers, LC is also a promised land. The interest rate on the platform is lower than the bank personal loan, and the process is as simple as applying for a credit card. The borrower can get the loan within a few days after he signs up.

In 2007, LC officially debuted on the Facebook platform. The strategy of using social graphs to make loans has attracted a lot of investors, and the company quickly got $10 million in financing.

At that time, LC had not disclosed the information of internal member loans, but still used it to prove its own performance. In 2010, Laplanche said that the company's yield reached 9.8%, surpassing rival Prosper. This low-risk but high-yield image has also attracted many investors for the company. Some large investors started to set up private equity funds and purchased large amounts of LC loans. In 2012, former Morgan CEO John Mack and former U.S. Treasurer Larry Summers joined the LC board.

LC listing, picture from cnbc

From the background, Laplanche himself is also a great candidate to subvert the traditional banking industry. He worked in a law firm in his early 20s and later co-founded a software company, Triple Hop Technologies, and sold it to Oracle in 2005.

Laplanche's motivation for starting LC was out of consideration: Why save money in the bank only get 1 point of interest, but if you use the same money, you have to pay 18 points of interest? So he thought, if there is a way to be able to make another loan borrowing between users, make cash flow more easily and quickly.

Today, LC has handled more than 1.6 million loans worth about $20 billion.

A query

LC publishes loan information on a daily basis, which includes anonymous borrower information. It was this information that caught the attention of Bryan Sims. He was once an entrepreneur and later became an investor in the LC platform and he fully invested his pension. When LC went public in 2014, Sims purchased its home stock and often listened to the company’s earnings report. In 2015, he heard from CEO Laplanche in a report that 14% of borrowers (about 100,000) had a second loan. This number makes Sims very curious because the repeat data company has never announced it.

So he decided to check the information about his own loan. The information included loan amount, interest rate, borrower salary, income, credit score and other information. There were two loans that made him curious because the borrower had the same employer and location. In addition, the income was basically the same, and the first credit was made at the same time. Sims realized that they may be the same person. The same person has two loans, but LC thinks they are not related and they charge different interest rates. The borrower's interest rate on the $15,000 loan is 15%, while the interest rate on the $30,000 loan is 9%. More importantly, LC seems indifferent.

Sims further discovered that LC's December 2009 data showed that 32 loans with a total value of more than $72 million were initially viewed from 32 people, but the main body was actually only 4 people. They changed information such as income and address. Borrow twice in 8 days. Twenty-nine loans were repaid within 90 days. These transactions are unusual, but nobody seems to notice.

Sims has two explanations for this. The first is identity theft. Someone may be testing new scams. The other explanation is conspiracy theory, that is, LC intends to falsify data. LC received $24.5 million in financing in April 2010, led by Foundation Capital. Sims believes that it is very likely that Laplanche or other executives want to use fake loans to make their business more beautiful before financing.

It turns out that Sims's guess is correct. LC later stated in a disclosure that in December 2009, Laplanche and three family members made 32 loans, and the total amount was the same as that of Sims. According to LC, the move was "to increase the loan volume of the platform in December 2009" and claimed that there were no other improper loans.

Sims also found that LC allowed borrowers to split their loans into two operations between 2009 and 2011, and there are thousands of such examples. For example, in June 2011, a user wanted to loan 25,000 U.S. dollars, but his FICO score was only 700 years earlier, which was a high risk type. At the time, the interest rate given by LC was 18%, and later the user received only about $20,000 in loans. But soon after, the same person borrowed about US$5,000 more, and the interest rate was 7.5% (it may be that the amount became less and the risk was reduced accordingly). From the outside, this seems to be a high-risk and a low-risk loan, but in fact the two risks are as high.

Sims issued a total of 30,000 loans suspected of having duplicate borrowers, but LC never published relevant information. This kind of information is very important to investors because borrowers may use multiple financial platforms at the same time, and the data can reveal how big the risk is.

Renaud Laplanche, picture from forbes

Unspoken rules

These things sound very unlikely, after all, LC is one of the most prestigious companies in the industry. The company's investors and board members are also renowned in the industry, and Laplanche himself has also been in a "white shoe company" (referring to operating A century-long Fortune 500 company has served as a securities lawyer.

But after the executives left the company, the company received a summons from the Justice Department and faced the SEC investigation. Once the second largest shareholder, Baillie Gifford, sold all the LC stocks, and after a series of LC layoffs of 12% in June, the situation may be better than expected. Worse still. The market value of LC was about 10 billion U.S. dollars, and now it has evaporated 80%.

Earlier LCs used social graphs to win financing, but few people on social platforms borrowed money openly. So according to Salil Deshpande, an early investor in LC, there was a need to do something “unnatural†to generate a deal. One of them is to encourage employees and relatives to make loans on the LC platform, and Deshpande does not think this is illegal.

It can be seen that LC also does not deny internal transactions, but thinks this is nothing new. As the company's C-round investor Charles Moldow said, this behavior is like attracting other users. It will invite friends to participate in activities. Informed sources told Bloomberg, internal staff loans is very common in the early LC. LC also previously stated that it had banned loans from directors and senior executives in 2008, and this limit was extended to all employees in 2010.

Silicon Valley also seems to be advocating this deception strategy, especially in the early stages of the career, which is also known as "growth hacking" to generate "potential energy."

An important company

The inaction on repetitive borrowers may be because LC collects fees from borrowers and lenders for profit, and it does not have much incentive to restrict recurring loans.

LC's model is to connect the borrower with the lender, although it uses its own risk control model to reduce the cumbersome loan process, but this does not guarantee to attract high-quality loan customers, and its loan cost is not cheaper than the bank. This makes it easier for LC to attract individuals or small businesses that do not meet bank loan standards, and it also exposes lenders to greater risks. For example, 70% of LC's business comes from helping customers repay credit card debt.

Not everyone can borrow on LC. In 2010, the borrower's FICO score must be higher than 660. This criterion is high enough. At that time, the demand from investors exceeded the demand of the borrower. As a result, LC even began to no longer verify income information for most borrowers. The reason is that the quality of unverified loans is as good as that of verification. This statement is not wrong, after all, US credit card applications rarely verify revenue information, but banks will verify fixed-rate loans. In any case, LC's claimed stricter standards than traditional banks have not been strictly enforced, which also allows high-risk individuals to come in and go.

Insiders said that as early as 30 years ago consumer finance in the United States covered almost 80% of consumers, new loan models may not be able to attract traditional customers. In contrast, 70-80% of consumers in China still do not use consumer financial services, and many of them are not using traditional financial services and are willing to try new high-quality users. Does this mean that P2P lending will start in the West, but in the East? After all, the market value of the domestic P2P lending platform is appreciably approaching LC.

Scott Sanborn, the new CEO of LC, believes that these events in the past are isolated and emphasizes that the company is retraining employees and will allow everyone to focus on the right things. As a successor, Sanborn has shown a positive side. He believes these issues are temporary and the company is back on track. Many investors still buy loans on LC, although trading volume has decreased. The amount of loans handled by the company in the last quarter also reached nearly 2 billion U.S. dollars, and there are still 500 million U.S. dollars in cash.

However, once the user’s trust in the platform is destroyed, it will be difficult to recover. Since the CEO can also participate in the scandal, then how to ensure the safety of investors? What's more, LC's role is essentially an intermediary and there is no capital protection service. When there is a breach of contract, the lender will have to bear its own investment losses and LC will not pay compensation.

LC is indeed the most important company in the financial technology field. It brought innovation and brought a serious credit crisis.

Air Core Inductor Coil,Ferrite Core Coil,Winding Air Core Inductors,Copper Induction Coil

IHUA INDUSTRIES CO.,LTD. , https://www.ihua-transformer.com